Fossil AI I—Finance Capital's New Utility Frontier

Private equity, utilities, and regulators gamble on plausibly exaggerated data center forecasts and long-lived fossil assets

{kind=link}

Over the past year, the financial press now routinely links the data center construction wave to broader fears of an AI bubble, extending beyond tech equities into power markets and infrastructure finance. At the same time, analysts estimate that global AI infrastructure spending could reach trillions of dollars over the next five years, a substantial share of it financed with debt on the assumption of robust and enduring cash flows. A survey of major fund managers reported that many institutional investors believe firms are overspending on AI infrastructure. The global head of digital Infrastructure for KKR even cautioned clients to “look beyond the bragawatts”: to treat headline announcements of data center capacity less as evidence of guaranteed demand and more as marketing in a crowded capital-raising environment. The warnings echo earlier technology booms where future growth was capitalized long before it was realized.

A second strand of reporting follows this logic downstream into utilities and data center operators. In the United States, utility stocks rallied on the back of an AI-power narrative that promised decades of rising demand and guaranteed cost recovery through ratepayers. That rally has already shown signs of strain as “AI bubble” concerns mount. Analysts now warn that if the most aggressive electricity demand scenarios fail to materialize, utilities will find themselves overvalued and holding stranded generation, pipelines, and grid upgrades built for a load that never arrived. Data center executives, for their part, publicly acknowledge the risk. Profiles of firms in India and Europe describe executives trying to “thread the needle” between capturing AI-related growth and avoiding overbuilding in what they frankly characterize as a “bubbly” market.

A series of widely syndicated Associated Press pieces has brought these concerns into the public regulatory arena. One article highlights “eye-popping” claims by U.S. utilities that they will need two to three times more electricity within a few years to serve new AI data centers, and asks whether these forecasts are padded with projects that will never break ground. Another reports growing skepticism among lawmakers and regulators in states such as Pennsylvania, Texas, and Ohio about whether speculative data center deals should be embedded in “base case” forecasts at all. Grid Strategies, a consultancy closely watched in energy circles, estimates that utilities now project roughly 90 gigawatts of added data center load by 2030—equivalent to nearly 10 percent of anticipated U.S. peak demand—while independent market analysts place a more realistic figure in the 60–65 gigawatt range. The wedge between those numbers represents not just methodological disagreement, but a vast volume of potentially overbuilt infrastructure.

Forecasts have also been revised upward with startling speed. BloombergNEF’s estimate of U.S. data center demand by 2035 has jumped by more than a third in a short period, and similar upward revisions are now steering plans for multi-billion-dollar generation, transmission, and pipeline investments. Advocacy and research groups such as IEEFA and As You Sow warn that utilities and private developers are using these exaggerated projections to justify a new wave of fossil gas plants and related infrastructure, even as the technical trajectory of AI remains deeply uncertain. The industry itself concedes that substantial gains in hardware efficiency, changes in model architecture, or a slowdown in training could sharply reduce load growth. Yet, in practice, today’s high-end forecasts are often treated as inevitabilities rather than contingent scenarios.

This combination of exuberant projections, rapid forecast inflation, and willingness to treat speculative demand as a planning baseline is the core problem. AI and data center loads are growing, but the financial and policy discourse around them is increasingly wrapping real technological change in a narrative that licenses overbuilding of fossil-based energy and socializes risks of a downturn.

This is part I of a multipart series. See part II on petrodollars and the AI infrastructure boom.

Private equity is using the AI boom to fuse data centers with fossil-heavy energy portfolios

If financial journalism frames AI infrastructure as a potential bubble, private equity and infrastructure funds treat it as an opportunity to reshape control over energy systems. Their pitch to clients is deceptively simple: AI, data centers, and electric vehicles will drive a structural surge in electricity demand; grids are constrained; therefore, owning flexible, dispatchable power is the surest way to capture the upside. Even worse—the narrative often launders an “energy transition” narrative that functions, in practice, as a strategy to lock in and revalue fossil assets under a variety of rationales from economic competitiveness and national security to the inevitability of technological revolution.

Let’s take Energy Capital Partners’ 2023 ESG report (which it calls “A Responsible Approach to Value Creation”) as an example—though many other investment firm reports are equally representative of the broad narrative framing. It presents the rise of AI, data centers, and EVs as a naturalized, quasi-inevitable source of load growth. That demand is not framed as the outcome of strategic corporate choices, regulatory decisions, and public subsidies, but as a kind of secular force to which investors must adapt. On that basis, the firm defends a “balanced portfolio” in which long-lived gas (and even coal) assets are recoded as responsible contributions to grid reliability in an era of AI-driven strain and interconnection bottlenecks. The effect is to turn what might otherwise appear as aging, carbon-intensive plants into future-proofed infrastructure keyed to a glamorous new demand narrative.

BlackRock’s recent moves demonstrate the scale at which this logic is being pushed. Its $12.5 billion acquisition of Global Infrastructure Partners (GIP), followed by GIP’s roughly $40 billion purchase of Aligned Data Centers in partnership with Nvidia, Microsoft, xAI, and MGX, has effectively positioned BlackRock at the center of the AI infrastructure buildout. The firm now stands among the largest private owners of gas-fired power plants globally and is expanding its control over regulated utilities and generation assets through deals such as the $6.2 billion acquisition of Allete and advanced talks to acquire AES. Together, these moves would give BlackRock direct or indirect stakes in around fifty fossil-fuel plants with more than 30,000 megawatts of capacity across multiple countries.

By consolidating ownership of both AI data centers and the fossil-heavy power portfolios that feed them, BlackRock is not simply “responding” to AI demand—it is helping to coordinate how and where that demand is translated into concrete energy infrastructure. The firm’s strategy relies on a particular vision of the future: that AI load will keep rising, that regulators will tolerate continued dependence on fossil generation in the name of reliability, and that data centers will remain sticky, long-term customers willing to sign contracts that underwrite new plants or extend the life of old ones. In such a world, owning both the server halls and the smokestacks becomes a vertically integrated play for a fossil-fueled digital capitalism.

Other asset managers are pursuing similar paths, stitching together portfolios of data center capacity, gas plants, and transmission assets under the rubric of ‘supporting the AI revolution.’ In early 2025, Blackstone announced its purchase of the 744-megawatt Potomac Energy Center gas plant in Loudoun County, Virginia—“Data Center Alley,” home to more than 130 data centers and roughly a quarter of global data center capacity. The firm explicitly described the acquisition as part of a strategy to back power infrastructure serving data centers and AI, calling it one of its “highest-conviction areas.” The plant is thus reimagined as a critical asset in a global digital hub, its future profitability secured by the presumed inevitability of AI expansion.

These are part of a string of large-scale partnerships. KKR and Energy Capital Partners have announced a $50 billion strategic partnership to invest in data centers and power generation linked to AI growth. A consortium including KKR and PSP Investments has taken a nearly 20 percent stake in transmission companies serving Midwestern states, tying high-voltage infrastructure more closely to private equity’s AI thesis. Brookfield has unveiled a $5 billion “AI infrastructure” partnership with Bloom Energy and joined with Cameco and the U.S. government in an $80 billion deal leveraging Westinghouse nuclear technology. Together, these deals map a coordinated effort to build portfolios in which AI demand is the justificatory glue binding fossil-heavy generation, nuclear assets, transmission networks, and hyperscale data centers into a single investment narrative.

In effect, AI is a marketing device that bundles old and new infrastructure into a single growth frontier for finance capital. But the assumption that AI workloads will reliably fill gigawatts of capacity for decades is exactly what analysts and regulators are beginning to question—and those doubts come into sharpest focus in utility planning.

Utility planning models are turning speculative AI demand into public obligations for new (fossil-heavy) capacity

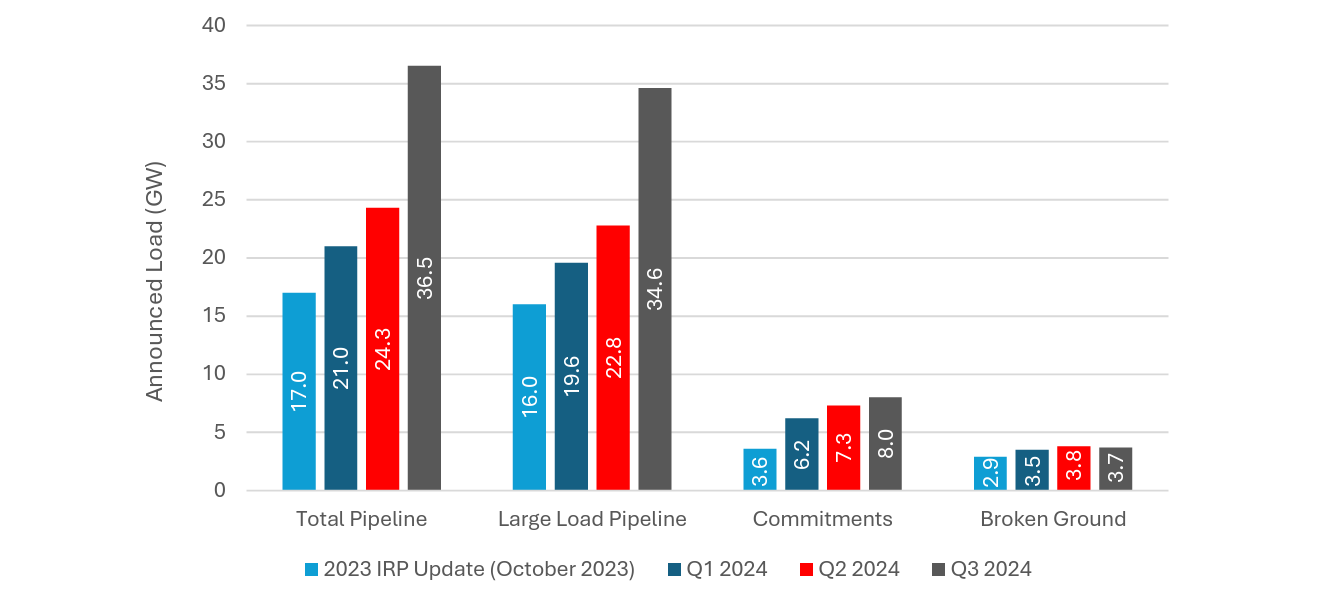

In Georgia Power’s 2025 Integrated Resource Plan, probabilistic hype about data centers is converted into a concrete build-out. Between its October 2023 IRP update and Q3 2024, its projected “Large Load Pipeline” grew from 16 GW to 34.6 GW, with 8 GW now coming from customers that have formally committed. This is a sharp revision from its 2023 plans, with the majority attributed to AI-oriented data centers. To meet this, the near- and medium-term portfolio is anchored in new and extended gas units and legacy coal, supplemented by battery storage, incremental nuclear uprates, hydro modernization, and a largely RFP-driven expansion of solar and wind. At stake is how a highly uncertain wave of AI and data center demand is being operationalized inside the IRP—and, in particular, how Georgia Power’s load forecast and its Large Load Realization Model are used to justify this new tranche of infrastructure.

On May 5, 2025, expert testimony poked holes in Georgia Power’s 2025 IRP load forecast—the projection it uses to justify new power plants and grid upgrades—and, specifically, its Large Load Realization Model. The expert witnesses accepted the broad architecture of the model but demonstrates that its innards are biased toward overestimation. Short-term commercial demand models have systematically overshot actual usage, and these inflated figures are then propagated into longer-term projections, baking excess into the planning process. The evidence is concrete: Georgia Power’s 2024 summer peak came in significantly below what its 2025 forecast had anticipated, even as the company cited rising AI and data center loads as reasons to accelerate capacity additions.

The sharpest critique focuses on how the model treats data centers. A “pipeline” of proposed large loads is used to estimate how many projects will ultimately connect to the grid. In the 2025 forecast, the model “unreasonably biases” the likelihood that data center projects will proceed, despite internal evidence that such projects cancel more often than other industrial loads (page 6, 51). By 2037, roughly 83 percent of the company’s large-load pipeline, measured on an announced-load basis, is made up of data centers. The forecast is therefore extraordinarily sensitive to the fate of a single volatile industry. Yet the model does not transparently account for higher cancellation rates, shorter contract terms, the shift from energy-intensive training to less demanding inference, or the possibility that many of today’s headline AI projects will never operate at full scale or for very long.

The testimony situates this modelling problem within a wider instability of AI-driven demand. It points to examples such as DeepSeek, a Chinese AI firm reportedly leaving up to 80 percent of its computing resources unused at times, and whose models are claimed to be far more energy-efficient than competitors. Industry analysts expect roughly a third of generative AI projects launched in the early wave to be abandoned or substantially scaled back by 2025 (page 78). With this in mind, building multi-decade infrastructure plans around the most bullish AI and data center scenarios begins to look less like prudent planning and more like a speculative gamble with public money. Nevertheless, in mid-2025, Georgia’s PSC voted to approve Georgia Power’s 2025 IRP.

*Georgia has adopted some ratepayer protections—primarily the PSC’s January 2025 large-load rule and a base-rate freeze approved just before the 2025 IRP—but a stronger statutory fix (see SB 34) has stalled, and other PSC decisions have simultaneously reduced transparency and left significant room for data-center costs to show up on bills later.

Across states, speculative AI load forecasts are colliding with growing regulatory pushback

As I’ve alluded to at the outset, Georgia is just one of many states in which this dynamic is playing out. GridUnity’s CEO reports that one large utility client saw roughly 30 percent of big-load proposals cancelled in 2024. A Grid Strategies report found that utilities in states such as Virginia, North Carolina, South Carolina, and Georgia have filed demand forecasts tied to data centers that exceed independent industry assessments by as much as a factor of four.

Despite this, the underlying AI business model remains far from settled. Scrutiny of OpenAI’s finances suggests that even the largest AI firms may struggle to grow revenues quickly enough to cover their enormous compute and infrastructure costs, especially if capital markets tighten. With early signs that the broader AI boom is slowing, doubts are rising about whether today’s aggressive load forecasts will ever translate into sustained, billable demand.

There is notable pushback. In Virginia, multiple parties have challenged Dominion Energy’s IRPs for leaning heavily on data center-driven growth. The Piedmont Environmental Council’s testimony shows that residential bills in 2039 could vary by about $100 per month depending on whether the projected data center load actually materializes, while independent reviews describe Dominion’s assumption that data centers will consume more than 80 percent of commercial sales and over half of total sales by 2038 as “improbable.”

Elsewhere, commissions are experimenting with ways to reinsert uncertainty into planning. In Oregon, proceedings on Portland’s fast-growing data center cluster emphasize the need for explicit high, reference, and low load cases. PacifiCorp’s 2025 IRP goes further, explicitly excluding certain large data center loads from its main retail forecast on the premise that those customers will procure and pay for their own dedicated resources—a move enabled by recent legislation on “large new loads” in Oregon and Utah. Kentucky’s Public Service Commission is using tariff design as a brake: expert testimony supports an “Extremely High Load Factor” rate for mega–data centers, paired with collateral and exit fees, as a precondition for approving new infrastructure built on anticipated demand. In California, staff and intervenors in IRP proceedings have begun citing research and journalism on AI data centers’ bill and blackout risks as they question how much speculative AI load should drive long-term procurement.

These cases show a regulatory field in tension. On one side are utilities and financiers eager to convert AI projections into concrete assets and regulated revenue streams—on the other are advocates, analysts, and some commissions insisting that AI load must be treated as contingent.

Can we avoid a stranded, fossil-heavy grid? Or is this the beginning of a fossil-fueled AI boom?

Throughout all of these developments, AI and data center loads are being invoked as an inevitability in order to justify a rapid, capital-intensive expansion of largely fossil-based energy infrastructure. Financial markets increasingly recognize the bubble-like features of this expansion, even as private equity and infrastructure funds use the AI story to revalue fossil assets and consolidate control over electricity systems. Within utilities, generous assumptions about data center realization rates and long-term AI demand are being embedded into planning models, transforming speculative forecasts into obligations to build plants, lines, and pipelines whose costs will fall on ratepayers for decades.

The question is not whether AI will use more energy—it clearly will—but who bears the risk that its most exuberant projections prove wrong. A more cautious, genuinely transitional approach would treat AI load as deeply uncertain, require robust high–medium–low scenarios, and insist that large data center customers shoulder a meaningful share of the financial risk through tariffs, collateral, and off-balance-sheet procurement. It would treat efficiency, demand management, and genuinely low-carbon generation as preconditions rather than afterthoughts. Above all, it would resist the seduction of inevitability that turns contingent corporate strategies into excuses for locking in fossil-heavy infrastructure under ambiguous allusions to “innovation” or “competitiveness.”

Thanks for explaining such a complex topic

This is an unusually clear account of how contingent demand gets laundered into institutional inevitability.

One structural layer worth emphasizing is that once forecasts become coordination anchors for capital, regulators, and utilities simultaneously, no single actor retains the legitimacy to downgrade them without appearing to “break the future.”

At that point, overbuild isn’t driven by belief so much as by coordination lock-in: everyone knows the projections may be inflated, but deviating unilaterally carries political and financial penalties.

AI here functions less as a technology and more as a narrative stabilizer that allows long-lived assets to be justified in advance of proof.