Will the Supreme Court Enable a New Era of Executive and Monopoly Power?

How a fight over FTC removal power could reshape federal control over energy, infrastructure, and the firms building the AI economy

A Supreme Court case about firing an FTC commissioner has become a test of whether the executive branch can discipline the independent commissions that govern AI’s two most important bottlenecks: monopoly power over compute and regulatory control over the energy systems needed to run it.

In March 2025, President Donald Trump fired Rebecca Kelly Slaughter from the Federal Trade Commission (FTC). Slaughter was not a cabinet secretary or White House adviser. She was an FTC commissioner serving a fixed statutory term. Trump had first nominated her to the commission in 2018. President Biden later renominated her, and her current term was scheduled to run until September 2029. The removal notice did not accuse Slaughter of corruption, incompetence, neglect of duty, or misconduct. It said her continued service was “inconsistent with my Administration’s priorities” turning the firing into a direct challenge to the legal structure of independent commissions. Under the FTC Act, commissioners may be removed only for “inefficiency, neglect of duty, or malfeasance in office.” Trump’s letter treated disagreement with the administration’s priorities as enough.

Slaughter sued. A federal district court held that the removal was unlawful and ordered the government not to interfere with her service. The D.C. Circuit declined to pause that ruling. The Trump administration then went to the Supreme Court, asking the justices to decide whether the FTC’s removal protections violate Article II and whether the Court should overrule Humphrey’s Executor, the 1935 precedent that upheld Congress’s authority to protect certain independent commissioners from at-will presidential removal. The case first appears to concern the FTC: antitrust enforcement, consumer protection, platform regulation, and presidential control over the administrative state. But one of the most important filings came from a different part of the federal regulatory system. Ari Peskoe, on behalf of a bipartisan group of former commissioners from the Federal Energy Regulatory Commission (FERC), filed an amicus brief warning that a decision against Slaughter could also unsettle the legal foundation of independent energy regulation.

FERC does not police deceptive advertising or investigate tech mergers. It regulates interstate energy systems. Its decisions shape wholesale electricity markets, transmission access, natural gas pipeline rates, oil pipeline rates, grid reliability, hydropower licensing, LNG terminals, and cost allocation for energy infrastructure. According to the former commissioners’ brief, FERC-set rates help finance roughly $40 billion in new energy-delivery infrastructure each year. More than $1 trillion in oil, gas, and electricity moves through infrastructure dependent on those rates. As the brief puts it: “FERC is to the nation’s energy system what the Federal Reserve is to its banking system.” FERC-regulated tariffs set the terms on which most U.S. energy is transacted at wholesale, govern interstate pipelines and power lines financed through FERC-set rates, and shape “energy system planning, operations, and trading.” The result is not only price regulation. “Taken together, FERC shapes our physical energy system and influences the quantity and types of energy produced in our country and delivered around the world.”

The former commissioners were not defending agency independence as a matter of institutional nostalgia. They were describing the regulatory machinery that governs industries built around monopoly power, public dependence, and long-lived private investment. Congress designed commissions such as FERC to keep those systems from falling under direct presidential command or private corporate discretion alone. Their independence has never made them apolitical. It has given regulated industries, consumers, states, and public advocates a venue where infrastructure decisions must be justified through records, rates, hearings, dissents, and statutory standards.

That structure now sits directly in the path of executive authority in the Trump-era, including the implementation of AI industrial policy. The administration has made “speed to power” a central objective for AI development. Hyperscale data centers need enormous quantities of electricity, often in the hundreds of megawatts. Their developers need land with access to substations, transmission lines, transformers, gas turbines, power contracts, backup generation, and interconnection approvals. Those needs do not move through the market alone. They pass through regulatory institutions.

FERC decides many of the rules that determine whether large AI loads can connect quickly, whether co-located power plants can reduce transmission obligations, whether gas and coal infrastructure can be treated as AI-enabling infrastructure, and whether ordinary ratepayers absorb part of the cost. The same Supreme Court case that asks whether Trump can fire one FTC commissioner therefore reaches into the agencies that govern the material basis of AI expansion. It links monopoly power in the AI economy to the energy systems needed to run it. From this perspective, Slaughter’s firing is more than a personnel dispute. If “policy disagreement” (to be generous) becomes a valid reason to remove independent commissioners, then agencies built to mediate conflicts over market power and infrastructure costs become easier to discipline from the White House.

Trump-era AI policy depends on FERC because “time to power” is now the industrial bottleneck

The Trump administration has made the link between AI and energy infrastructure explicit. In July 2025, the White House issued an executive order to accelerate federal permitting for data center infrastructure. The order defined a “Data Center Project” as a facility requiring more than 100 megawatts of new electricity demand for AI inference, training, simulation, or synthetic data generation. It then defined the infrastructure needed for those projects broadly—high-voltage transmission lines, natural gas pipelines and laterals, substations, switchyards, transformers, switchgear, gas turbines, coal power equipment, nuclear power equipment, geothermal equipment, backup power, semiconductors, networking hardware, and data storage. AI data centers depend on “infrastructure that powers them.”

The same order folds permitting, finance, and national-security designation into one process. A qualifying project can be a data center or component project with at least $500 million in capital expenditures, a project adding more than 100 MW of electric load, a project that protects national security, or a project designated by the secretaries of defense, interior, commerce, or energy. Agencies are directed to ease regulatory burdens and support rapid buildout on federal land and other sites. In practice, AI is less a software sector than a territorial program—large parcels, power equipment, public finance, transmission access, environmental review, and federal coordination assembled around the demand for computation.

FERC enters because the main constraint is no longer whether firms want to build data centers. They do. The harder question is whether they can energize them quickly. A data center site without firm power is only a real estate option. “Firm” power means electricity service the user can count on rather than power that may be interrupted whenever the grid tightens. A large AI campus also needs a place in the interconnection process, which is the technical and legal review that determines whether a new user can connect to the grid, what equipment must be upgraded, and who pays for those upgrades. “Time to power” has become the practical measure of whether an AI project can move from announcement to operation.

Read more detail on this here:

The Department of Energy’s October 2025 letter to FERC puts that problem into regulatory language. Secretary Chris Wright wrote that large loads, including AI data centers, must be able to connect to the transmission system in a “timely, orderly, and non-discriminatory manner.” In electricity regulation, “load” means demand: the amount of power a customer draws from the system. The DOE proposal defined large loads as those above 20 MW, which is small compared with the largest AI campuses but large enough to affect grid planning. The letter urged FERC to consider reforms that would speed studies for certain projects, examine whether some studies could be completed within 60 days, and require large loads and hybrid load-generation projects to pay for assigned network upgrades.

That proposal marks a significant shift. FERC has long focused its interconnection rules on generators—power plants, wind farms, solar projects, batteries, and other resources that inject electricity into the grid. Data centers invert the problem. They withdraw power at a scale that can resemble a major generating station in reverse. A single large campus can demand hundreds of megawatts; at one thousand megawatts (a gigawatt), it reaches the scale of a major power plant. If those loads wait in ordinary planning queues, projects slow. If they receive faster treatment without strong cost rules, other customers can inherit reliability risks, grid-upgrade costs, and higher bills (as Peskoe and Martin warned earlier). FERC’s large-load docket therefore turns AI industrial policy into grid law: it asks how hyperscale demand should enter a transmission system built around public-service obligations, not just private speed.

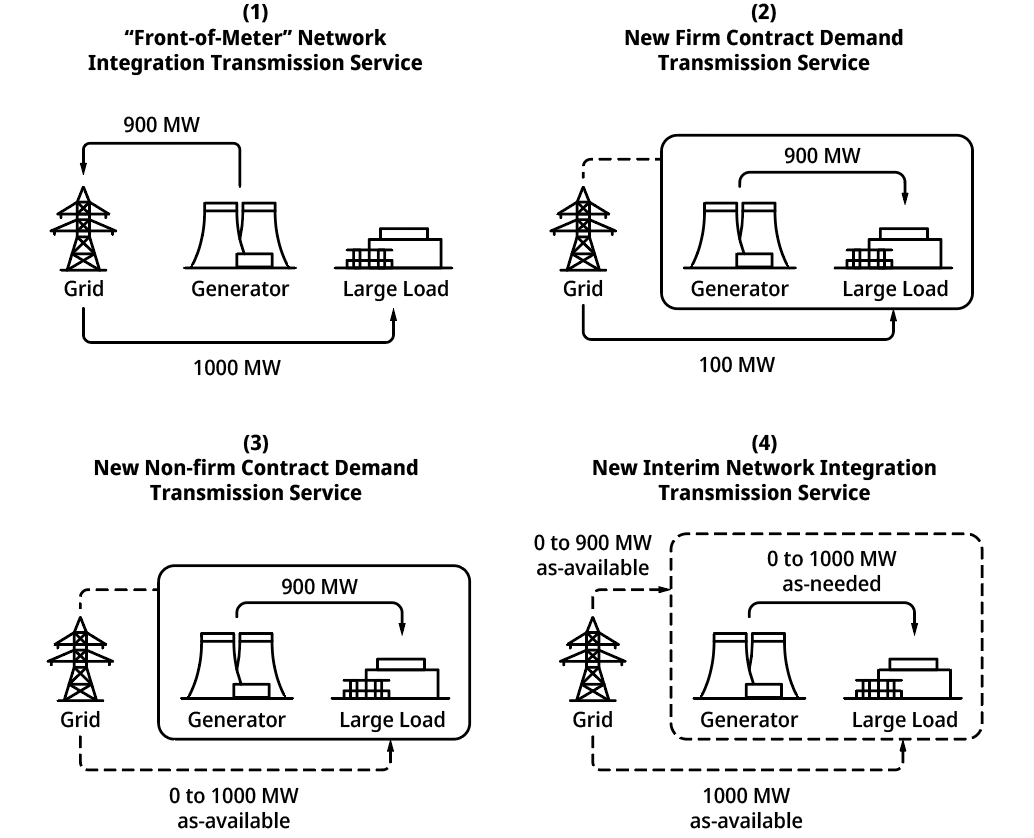

FERC’s co-location order to PJM gives us a clear sense of where things are headed. PJM is the country’s largest grid operator, serving the Mid-Atlantic and parts of the Midwest, including the region around Northern Virginia where data center growth has been most intense. A grid operator coordinates electricity flows, runs wholesale markets, and manages reliability across utility territories. In December 2025, FERC ordered PJM to revise its tariff, the rulebook that governs charges and service terms, for data centers and other large loads located near power plants. FERC said PJM’s existing rules were unclear over the rates, terms, and conditions that apply when generation and load sit together.

Co-location is the core strategy here. If a data center sits beside a power plant, the developer can argue that it does not need the same amount of transmission service as a conventional customer drawing all of its power from the wider grid. Commissioner David Rosner’s concurrence gives a simple example. If a new 1,000 MW generator sits beside a new 900 MW data center, the generator could “reserve” 900 MW to serve that data center directly and request permission to inject only the remaining 100 MW onto PJM’s grid. Studying the project at the smaller net injection could reduce required transmission upgrades and move power online faster. Rosner summarized the policy effect as making “bringing your own new generation” cheaper and faster.

The same arrangement can also work from the load side. A data center located beside a generator may claim that it draws less from the regional grid than its full nameplate demand suggests. Nameplate demand is the maximum amount of power a facility is designed to use. Net demand is what the wider grid must supply after accounting for nearby generation. Since transmission costs often follow measured reliance on the shared system. A data center that can present itself as partly self-supplied may pay less for transmission upgrades, move through studies faster, and look more financeable to investors.

That efficiency claim has a public-cost problem. Commissioner Judy Chang warned that co-located loads may still depend on the grid even when they buy little formal transmission service. Their generators remain synchronized with PJM, which means they rely on the grid’s stability, frequency, reserves, and emergency services. Without that connection, they would be separated from the wider system and forced to operate as a self-contained electrical network. Chang noted that one proposed service framework could leave some co-located loads paying only black-start and regulation charges. Black-start service keeps the system capable of restarting after a major outage. Regulation service balances tiny second-by-second mismatches between supply and demand. Chang’s concern was that these limited charges do not necessarily cover the cost of building, operating, and maintaining the grid.

In effect, FERC’s co-location rules could let data centers get power faster and more cheaply by pairing with nearby power plants, but if they pay only for regulation and black start services, they would be covering charges that averaged about $159 million and $47.5 million in PJM, compared with $10.81 billion for transmission (estimates by PJM Independent Market Monitor for January through September 2024 and 2025), meaning they may pay for less than 2% of the grid-cost category they still rely on while avoiding much larger shared transmission costs.

Reuters described the industrial meaning of FERC’s order more bluntly. Analysts called it a “major victory” for existing gas and nuclear plants because it creates a path for power plants to reduce deliveries to the grid and serve behind-the-meter customers such as data centers instead. “Behind the meter” means electricity is consumed on-site or through a direct arrangement rather than sold first into the broader grid as ordinary wholesale power. Reuters also reported that PJM capacity prices had risen by about 1,000 percent over roughly two years as Big Tech data center demand tightened the regional power market. Capacity prices matter because customers pay generators not only for electricity produced, but also for being available when needed. When expected demand rises quickly, those availability payments can surge.

This is the arena in which FERC has become central to AI policy. The commission is not deciding whether AI is useful, whether models should be trained, or whether companies can buy land. It is deciding how claims on electricity become legitimate, bankable, and chargeable. It determines how co-located load counts, how much transmission service a data center must buy, how interconnection studies proceed, how grid dependence is measured, and how costs move between developers, utilities, generators, and the public. AI firms and infrastructure developers are therefore searching not only for cheap acreage but for powered land: sites where land, generation, transmission, gas supply, and regulatory rules can be assembled into a durable claim on electricity. The politics of AI buildout in part runs through those technical decisions.

The fight over independent commissions reaches monopoly power and fossil energy

The fight over Slaughter’s removal turns on a distinction that sounds legalistic yet its institutional consequences are considerable. Presidents already shape independent commissions. They nominate commissioners, designate chairs, influence budgets, issue executive orders, and coordinate policy through cabinet agencies. But agencies such as the FTC and FERC were designed so that commissioners do not serve as ordinary presidential subordinates. They sit for fixed terms, the seats are staggered across administrations, and statutes allow removal only “for cause,” which means a commissioner can be removed for misconduct, neglect, or incapacity, not for casting the wrong vote.

The Supreme Court’s September 2025 order put that distinction at risk. The Court stayed the district court ruling that had protected Slaughter and agreed to decide whether FTC removal protections violate separation of powers and whether Humphrey’s Executor should be overruled. Justice Elena Kagan’s dissent described the agencies involved in these cases as “classic independent agencies”: “multi-member, bipartisan commission[s]” whose members serve staggered terms and cannot be removed except for good reason. She warned that the Court’s emergency orders had “handed full control of all those agencies to the President,” allowing him to remove members “for any reason or no reason at all.” If policy disagreement becomes enough, statutory independence no longer protects regulatory judgment.

FERC’s personnel story shows why that question now matters for energy. In October 2025, Trump named Laura Swett chair of the Federal Energy Regulatory Commission. FERC’s announcement says Swett had litigated FERC law for 15 years, including work representing “generating utilities, transmission owners, and natural gas and liquids pipelines,” most recently at Vinson & Elkins. Swett said she was grateful for Trump’s confidence and would advance “America’s energy priorities at such a critical moment in our Nation’s history” and later noted that her “number one priority is to make sure that American data centers can connect” while seeking to “eliminate uncertainty” through deregulation and co-location strategies. Furthermore, Swett said she would not recuse herself from pending proceedings involving data centers and a client of her former law firm. She also appointed James Dawson, a former Vinson & Elkins colleague, as FERC general counsel, and that Vinson & Elkins represented Talen Energy in proceedings involving a data center arrangement tied to the Susquehanna nuclear plant. FERC’s ethics official cleared Swett to participate in a major data center proceeding that could affect her former employer’s interests because of “the Government’s interest in her participation.”

The same problem appears at the FTC through monopoly rather than electricity. Under Lina Khan, the FTC investigated the large AI partnerships linking Microsoft and OpenAI, Amazon and Anthropic, and Google and Anthropic. The FTC used its Section 6(b) authority, a power that lets the agency gather nonpublic information for market studies rather than immediate litigation. Its January 2025 staff report found that these partnerships involved more than $20 billion in cumulative financial investment and substantial non-monetary exchange. A staff report warned that the arrangements could affect access to computing resources and engineering talent, raise switching costs for AI developers, and give cloud service providers access to sensitive technical and business information unavailable to others.

Those concerns go to the structure of the AI economy. Cloud service providers are the firms that own and operate large computing platforms like Microsoft Azure, Amazon Web Services, and Google Cloud. They sell access to servers, chips, storage, and networking capacity. Foundation model companies need those systems because frontier AI models require immense quantities of specialized computing power. When a cloud provider invests in an AI developer, sells it discounted compute, receives revenue-sharing rights, or gains privileged technical information, the relationship can become more than ordinary contracting. It can shape who gets access to scarce compute, who can afford to train models, and who becomes dependent on a dominant platform. One Cloud Service Provider (CSP), according to the FTC report, described information-sharing as a “multi-year crystal ball into the future needs of AI infrastructure” which can bear on data center siting decisions:

The Trump administration’s AI Action Plan moved against that regulatory posture. It says that “America’s private sector must be unencumbered by bureaucratic red tape” and directs officials to review all FTC investigations begun under the previous administration to ensure they do not advance theories of liability that “unduly burden AI innovation.” It also calls for review of FTC final orders, consent decrees (a negotiated legal order that binds a company without a full trial), and injunctions (a court or agency order requiring or forbidding specific conduct), with modification or set-aside where appropriate. The plan therefore reaches both pending investigations and completed remedies.

This is not a retreat of the state from the AI economy as the administration’s use of the term “deregulation” may suggest. It is a reorientation of state power. The FTC is pushed to avoid competition theories that might slow platform partnerships, cloud commitments, compute dependency, or AI consolidation. FERC is pushed to accelerate the energy arrangements that make large-scale compute possible. One agency governs market structure; the other governs material capacity. The FTC asks who controls models, cloud access, data flows, and compute contracts. FERC decides how electricity infrastructure is priced, sequenced, and made available to the largest new loads. AI industrial policy needs both forms of governance to move in the same direction.

Fossil energy benefits because AI demand gives coal, gas, and related infrastructure a new strategic language. The administration’s data center order treats natural gas pipelines, gas turbines, coal power equipment, nuclear power equipment, transmission lines, substations, transformers, and “dispatchable” baseload power as components of AI infrastructure. “Dispatchable” is doing important work here. In energy policy, it means power that can be called on when needed, rather than only when the “sun shines” or “wind blows”; in practice, the term often points toward gas, coal, nuclear, or other firm generation. Hyperscale AI loads need continuous, high-volume power. Some data centers will use renewables, batteries, or hybrid arrangements incentivized by speed to power under the Biden administration, but the Trump-era alliance has pushed the energy system toward existing coal plants, gas turbines, pipeline capacity, and market rules that let large loads pair with nearby generation.

Removal power connects these pieces. A commissioner considering a stricter cost rule for data centers, a tougher view of gas-backed co-location, or a broader antitrust theory for cloud-AI partnerships would no longer face only legal argument and evidentiary pressure. At-will removal would add executive discipline. Regulation would still use the language of reliability, consumer protection, competition, and innovation, but the acceptable range of conclusions would narrow. Slaughter’s case matters because it asks whether independent commissioners can still make adverse judgments when those judgments obstruct the preferred settlement among AI platforms, energy incumbents, and the administration’s industrial policy.

A new era of executive and monopoly power?

Independent commissions were created for sectors where monopoly power, private investment, and public dependence are inseparable. Electricity, gas pipelines, railroads, communications, and finance are not ordinary markets. They are the operating systems of economic life. Firms, households, universities, hospitals, factories, and governments cannot simply opt out of them. FERC’s procedures, including tariffs, rate cases, evidentiary records, dissents, and “just and reasonable” rate standards, force concentrated power to defend its claims on public infrastructure.

That structure matters because AI firms are not ordinary utility customers. Cloud platforms, chip companies, model developers, and infrastructure investors are consolidating control over compute, data, energy procurement, and the physical systems that make digital markets possible. The Trump administration has defined large data centers as strategic infrastructure and treated their energy needs as a national priority. Faster interconnection, co-location with power plants, fossil-backed firm generation, lighter review, and pressure on regulators all turn AI’s electricity demand into a privileged claim on the grid.

The Supreme Court’s decision on the Slaughter case, which could come in early to mid-June, will help determine whether independent regulators can still impose real limits on that claim. One path treats data centers as private industrial loads that must disclose their demand, pay for the upgrades they cause, and compete for power under rules that protect other users. The other treats AI as a strategic sector whose dominant firms can bend public systems around private buildout.

AI industrial policy is taking shape through tariff design, interconnection queues, pipeline certification, capacity-market rules, antitrust enforcement, commission appointments, and Supreme Court doctrine. These instruments determine how monopoly power attaches itself to energy, regulation, and the material base of computation. The larger question is not whether the state will support AI. It is whether public regulation will discipline the firms that control compute and energy access, or whether technological priority will discipline regulators instead. When monopoly power arrives as national necessity, agencies must still be able to say no, not yet, disclose more, or pay your share.

More reading on AI industrial policy and the emerging fossil-AI nexus:

{kind=link}